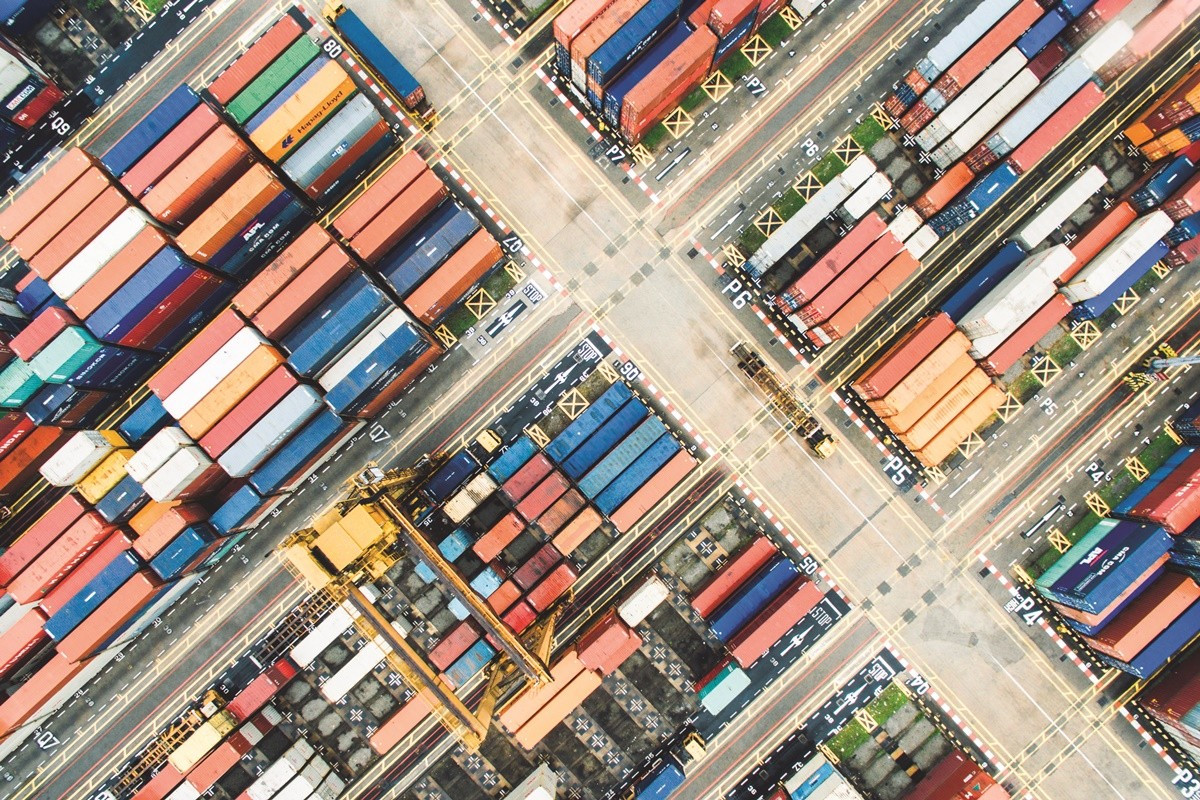

The state of supply chain and logistics is replete with both new and existing challenges

But one major difference between a year ago, at this time, when we were deep into the early innings of the pandemic, was that we were all lining up outside supermarkets to buy essential goods (during the few times anyone went outside); highways more or less deserted and airports empty; retail stores were shuttered or largely devoid of customers; manufacturing activity was largely shuttered; and everyone and anyone was buying whatever they needed online (that is still happening and is not going away), among other things.

Well, now roughly nine months later, there are clear signs things are improving in myriad ways. For one thing, people are receiving the COVID-19 vaccine, which has, in turn, led to economic reopenings in many parts of the country. For an economy that points to consumer spending for roughly 70% of its revenue, that cannot be overlooked. And it is being reflected in many key macroeconomic and freight-focused economic indicators, including retail sales, GDP, home sales; trucking and railroad and intermodal volumes, and, of course, import volumes.

All one needs to do is look at recent data from the Association of American Railroads or the American Trucking Associations, among other organizations, to quickly see how things have changed, for the better, in regard to these annual comparisons. While things are looking better on the freight flows and volumes front, there are many causes for concern, aside from the pandemic, that need to continue to receive a watchful eye.

Of course, many industry observers make the (correct) point to be comparing current volumes to 2019, the last full “normal” pre-pandemic year, for more of an apples-to-apples comparison.

These include things like the intersection of the elevated state of U.S.-bound imports and port congestion, especially in Southern California, a topic that has received a healthy amount of attention, for good reason. Another issue continues to be truckload capacity, as demand continues outweigh capacity, with rates continuing to benefit carriers. How long is that situation sustainable for shippers weighing their options? Time will tell, I guess.

What’s more, while things are improving, in terms of demand and a welcome return to more freight-focused activity, there continues to be a heightened sense of caution and an ongoing focus on risk management, for global supply chains, too. One example, of course, is the recent dislodging of the Ever Given vessel in the Suez Canal for upwards of a week, a situation that would have been even worse had it lingered for longer. And another is news over the weekend that the Colonial Pipeline, which accounts for nearly half of U.S. fuel supplies, fell victim to a cyberattack. That situation remains ongoing and will need to be closely watched.

When looking back at the state of the world, and, by extension, supply chain and logistics, there really is a lot to sort through. Not all of it is pleasant, but much of it ties back to our industry. Supply chain and logistics, despite their global scale, are often in the background and humming along during normal times, but given all that has occurred over the last several months, those days could well be part of the past.